When it comes to getting out of debt, choosing the right repayment strategy is crucial. Two of the most popular methods are the Snowball vs Avalanche method of approaches. Both have their own unique advantages and can be powerful tools in your journey toward financial freedom. In this article, we’ll explore how each method works, their pros and cons, and why personal finance expert Dave Ramsey is a strong advocate of the Snowball method due to its psychological impact.

The Snowball Method

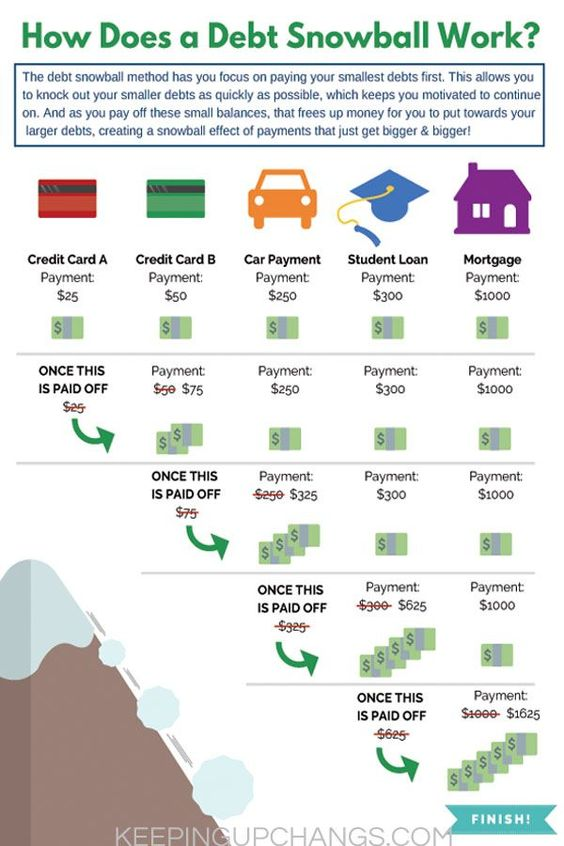

The Snowball method involves paying off your debts from the smallest balance to the largest, regardless of the interest rate. Here’s how it works:

- List Your Debts: Arrange your debts in order from the smallest balance to the largest.

- Make Minimum Payments: Pay the minimum amount on all debts except the smallest.

- Attack the Smallest Debt: Direct any extra money you can toward paying off the smallest debt as quickly as possible.

- Roll Over Payments: Once the smallest debt is paid off, move on to the next smallest debt, adding the amount you were paying on the previous debt to this one.

- Repeat: Continue this process until all debts are paid off.

Why Dave Ramsey Supports the Snowball Method

In discussing the benefits of the snowball method, Dave Ramsey, a well-known personal finance expert, often cites its psychological advantages—seeing debts disappear quickly can significantly motivate individuals to keep going. For more insights, you can visit Dave Ramsey’s official guide on debt repayment for detailed strategies and success stories.

According to Ramsey, the sense of accomplishment from paying off smaller debts gives people the confidence to keep going. This momentum, or “snowball effect,” can be incredibly powerful in helping people stay on track. As Ramsey puts it, “Personal finance is 80% behavior and 20% head knowledge.” The Snowball method aligns with this philosophy by focusing on behavioral change and creating a sense of progress.

Pros of the Snowball Method:

- Quick Wins: Paying off smaller debts first provides a psychological boost.

- Motivation: The momentum created by small victories can help maintain motivation.

- Simplicity: It’s easy to implement and understand.

Cons of the Snowball Method:

- Costly in the Long Run: You may end up paying more in interest compared to other methods.

- Ignores Interest Rates: The focus on balance size rather than interest rates can lead to higher overall costs.

The Avalanche Method

The Avalanche method, on the other hand, involves paying off your debts in order of interest rate, from highest to lowest. Here’s how it works:

- List Your Debts: Arrange your debts in order from the highest interest rate to the lowest.

- Make Minimum Payments: Pay the minimum amount on all debts except the one with the highest interest rate.

- Attack the Highest Interest Debt: Direct any extra money you can toward paying off the debt with the highest interest rate as quickly as possible.

- Roll Over Payments: Once the highest interest debt is paid off, move on to the next highest interest debt, adding the amount you were paying on the previous debt to this one.

- Repeat: Continue this process until all debts are paid off.

Pros of the Avalanche Method:

- Saves Money: Paying off high-interest debt first minimizes the total interest paid.

- Faster Payoff: This method often leads to quicker overall debt repayment, depending on your balances and interest rates.

Cons of the Avalanche Method:

- Less Immediate Satisfaction: It may take longer to see progress, which can be discouraging.

- Complexity: Requires more discipline and focus, as the wins may not come as quickly.

Which Method Should You Choose?

The decision between the Snowball vs. Avalanche method ultimately depends on your personal financial situation and mindset.

- If you’re someone who thrives on quick wins and needs consistent motivation, the Snowball method may be more effective. The psychological boost you get from knocking out small debts can keep you engaged and committed to your debt-free journey.

- If you’re more focused on minimizing costs and are comfortable with a more strategic, long-term approach, the Avalanche method might be the better option. By targeting high-interest debts first, you’ll save money in the long run and potentially pay off your debt faster.

Both methods have their merits, and there’s no one-size-fits-all answer. Some people even choose to combine elements of both approaches, starting with the Snowball method to build momentum and then switching to the Avalanche method to tackle higher-interest debts.

In the end, the best method is the one that keeps you motivated and moving forward. Whether you choose the Snowball or Avalanche method, the most important thing is to stay consistent and keep your eye on the ultimate goal: financial freedom.

Now that we are working on being debt free, what’s after? Take a look at our 401(k) article for information on how to best set yourself up for a successful retirement.

Pingback: The Power of Starting Your 401(k) Early and Letting It Grow - Wealth Sown